Tracking returns isn't the same as understanding your portfolio. Real analysis means checking concentration (no stock over 20-25%), sector exposure (no sector over 35-40%), correlation between holdings, and performance attribution to see if one winner is carrying everything. The post walks through a five-step process and shows how a portfolio of four mega-cap tech names plus cash looks diversified but is really 90% tech and one sector correction away from a ~27% drawdown. The real test of risk isn't your returns — it's whether you'd hold through a 25-30% drawdown without panic-selling.

- •Cap any single stock at 10-15% of your portfolio (20-25% absolute ceiling) and any single sector at 40%, even if you own many names within it.

- •Run a performance attribution check: subtract your top winner's contribution from your total return — if what's left trails the S&P 500, one stock is carrying you, not your strategy.

- •Pressure-test your risk tolerance by asking if you'd hold through a 25-30% drawdown; if not, reduce exposure now rather than during the correction.

How to Analyze Your Stock Portfolio (Step-by-Step Guide)

A clear guide to understanding portfolio risk, concentration, diversification, and performance drivers. Plus how AI makes it 10x faster.

Most investors track their returns, but very few actually understand what's going on inside their portfolio.

You might be up 10-15%, but:

- Are you taking too much risk?

- Are you overexposed to one sector?

- Are a few stocks carrying everything?

If you can't answer these questions, you're not really managing your portfolio. You're guessing. And most retail investors are guessing, because proper portfolio analysis has traditionally required spreadsheets, financial knowledge, and hours of work. Most people don't have time for it, so they skip it entirely.

This guide shows you how to analyze your portfolio properly, what to actually look at, and how to do it in minutes instead of hours.

What Is Portfolio Analysis?

Portfolio analysis means understanding how your investments work together, not just individually.

When you look at one stock, you're asking "is this a good investment?" When you analyze a portfolio, you're asking something different: "is this combination of investments working as intended?" A portfolio of ten great individual stocks can still be a bad portfolio if they all move together, leaving you exposed to the same risk ten times over.

Portfolio analysis focuses on four things:

- Risk: how volatile is your portfolio, and could you tolerate a 20-30% drawdown?

- Diversification: are your holdings actually spread across different drivers, or just different names?

- Concentration: are you relying on one or two positions for most of your returns?

- Performance drivers: what's actually making or losing you money?

The goal isn't just better returns. It's smarter, more controlled investing. A portfolio that returns 8% with half the volatility of the S&P 500 is often a better portfolio than one that returns 12% with double the volatility, especially if you'd panic-sell the second one in a downturn.

Quick Answer: How Do You Analyze a Portfolio?

The fastest way to analyze a portfolio is to check:

- Concentration: is any single position more than 20-25% of your portfolio?

- Sector exposure: is any sector more than 35-40% of your portfolio?

- Correlation: do your top holdings move in the same direction most of the time?

- Performance attribution: what percentage of your gains come from your top 3 positions?

- Risk vs. benchmark: is your portfolio more or less volatile than the S&P 500?

You can do this manually with a spreadsheet, or use tools to get instant insights. The rest of this guide walks through each step in detail.

Step 1: Check for Concentration Risk

Concentration risk is the most common issue in retail portfolios, and the easiest to fix once you see it.

If one stock dominates your portfolio, your results depend heavily on it. A strong rally boosts everything, but a single earnings miss or scandal drags your entire portfolio down. Concentration feels good on the way up and devastating on the way down.

Example: If Apple makes up 35% of your portfolio, Apple essentially is your portfolio. Apple's 20% drop is your 7% drop, from one stock alone.

Rule of thumb: No single stock should be more than 20-25% of your portfolio. For most retail investors, 10-15% is a better ceiling. If you inherited a concentrated position (from an employer stock plan, for example), consider reducing it over time rather than all at once, especially if you'd owe capital gains on the sale.

How to check: Add up the market value of your largest position and divide by your total portfolio value. If the answer is above 20%, you're concentrated.

Step 2: Look Beyond Returns

Returns alone don't tell the full story. A portfolio returning 15% might be extremely volatile, heavily concentrated, or riskier than you realize. A boring portfolio returning 10% with lower volatility might actually be the better portfolio.

Risk is usually measured with a few specific metrics:

- Beta: how much your portfolio moves relative to the S&P 500. A beta of 1.2 means your portfolio moves 20% more than the market in both directions.

- Standard deviation: how much your returns vary from their average. Higher standard deviation means more volatility.

- Max drawdown: the biggest peak-to-trough drop your portfolio has experienced. This matters because it shows what you'd actually have to sit through.

You don't need to calculate these yourself for casual analysis. But you should know they exist, because they're what separates a good portfolio from a lucky one.

The honest test: Imagine your portfolio dropped 25% tomorrow. Would you hold, buy more, or panic-sell? If the answer is panic-sell, you're taking more risk than you can actually tolerate, regardless of what your returns look like today.

Step 3: Evaluate Diversification Properly

Many investors think they're diversified, but aren't.

The most common mistake is holding multiple stocks that look different but move together. NVIDIA, Microsoft, and Amazon are different companies in different businesses, but they're all large-cap tech and they tend to move in the same direction during market cycles. Owning all three doesn't give you three times the diversification. It gives you three versions of the same bet.

True diversification requires:

- Different sectors: tech, healthcare, financials, consumer staples, energy, utilities. The S&P 500 is roughly 30% tech, 13% healthcare, 12% financials, 10% consumer discretionary, 9% communication services, and smaller allocations to the rest. Use that as a rough benchmark.

- Different market caps: large caps behave differently from small caps, especially during recessions.

- Low correlation: ideally, some of your holdings move independently from the rest. Bonds, international equities, and defensive sectors like utilities often have lower correlation with US tech.

- Different risk profiles: growth stocks and dividend stocks serve different roles in a portfolio.

How to check: Group your holdings by sector. If any single sector is more than 40% of your portfolio, you're sector-concentrated, even if you own many different stocks within that sector.

Step 4: Identify What's Driving Performance

Most portfolios are carried by a few positions. This is called performance attribution, and it's often the most revealing part of portfolio analysis.

Ask yourself:

- Which stocks contributed most to your gains this year?

- Which ones are consistently underperforming?

- If you removed your top winner, what would your return actually be?

Example: A portfolio might be up 18% year-to-date. Impressive, until you notice that NVIDIA contributed +12% of that return by itself. Without NVIDIA, the portfolio is up 6%, below the S&P 500. The portfolio isn't really outperforming. One stock is, and the rest are mediocre.

This is where real insight happens. You might discover:

- One winner is doing all the work, and if it stops, you have a problem

- Several positions are consistently underperforming and should be reassessed

- A stock you believed in is quietly dragging you down

- You're paying for positions that don't earn their place

Step 5: Review Your Allocation

Look at how your money is distributed across:

- Stocks vs. cash vs. bonds: if you're 100% stocks, you have no buffer during downturns. Most financial advisors suggest some cash position, especially for older investors.

- Growth vs. value: growth stocks (tech, biotech) perform differently than value stocks (banks, utilities) depending on the economic cycle.

- Domestic vs. international: US stocks are about 60% of global market cap, but 90%+ of most retail portfolios. Some international exposure reduces US-specific risk.

- Defensive vs. cyclical: consumer staples and utilities hold up in recessions. Consumer discretionary and industrials don't.

A well-balanced portfolio should align with your risk tolerance, your investment timeline, and your goals. A 30-year-old saving for retirement has different allocation needs than a 60-year-old nearing retirement.

Common Portfolio Analysis Mistakes

Avoid these:

- Focusing only on returns. A 20% return with 40% volatility is worse than a 10% return with 12% volatility, risk-adjusted.

- Assuming more stocks = diversification. Ten tech stocks is one tech bet, not ten bets.

- Ignoring sector concentration. You can be diversified by company and concentrated by sector at the same time.

- Never rebalancing. Portfolios drift over time. Winners grow, losers shrink. Without rebalancing, concentration builds automatically.

- Holding losers without reassessing. Not every losing position is a long-term opportunity. Sometimes the thesis was wrong. Be honest with yourself.

- Ignoring fees and taxes. A portfolio with high turnover generates taxable events. Compare after-tax returns, not just gross returns.

Example Portfolio Analysis

Consider this portfolio:

- 35% NVIDIA

- 25% Microsoft

- 20% Amazon

- 10% Tesla

- 10% Cash

At first glance, it looks reasonable. Four different companies and some cash. In reality:

- 90% is in stocks, 10% in cash: aggressive allocation with no bond buffer

- 90% of the stock allocation is in tech: extreme sector concentration

- 80% of the portfolio is in four mega-cap tech stocks: high correlation, all move together

- Performance depends almost entirely on large-cap tech continuing to outperform

- A tech sector correction of 30% would drag the portfolio down by around 27%

What a balanced version might look like:

- 15% NVIDIA

- 12% Microsoft

- 10% Amazon

- 8% Tesla

- 10% healthcare (e.g., Johnson & Johnson, UnitedHealth)

- 10% financials (e.g., JPMorgan, Berkshire Hathaway)

- 10% consumer staples (e.g., Procter & Gamble, Costco)

- 10% international (e.g., an international ETF)

- 15% cash and short-term bonds

Same total exposure to the top four tech names, but tech is now 45% instead of 90%, and the portfolio has real sector diversification and a meaningful defensive allocation.

What Should You Do After Analyzing?

Once you understand your portfolio, you can take action:

- Reduce overexposure: if any single stock is more than 20-25%, consider trimming it

- Rebalance across sectors: bring sector weightings closer to your target

- Add defensive positions: healthcare, consumer staples, or utilities if you're overweight growth

- Reevaluate underperformers: if a position has lost 30%+ and your thesis has changed, don't hold out of hope

- Set a rebalancing cadence: once or twice a year is enough for most investors

Why Manual Analysis Is Hard

Doing this manually requires tracking multiple metrics, comparing correlations, interpreting financial data, and understanding what the numbers actually mean. Most investors either skip it or oversimplify it. The result is portfolios that feel managed but aren't, full of hidden concentration, correlation, and risk that the owner can't see.

A Faster Way: Use AI

Instead of spending hours analyzing your portfolio in a spreadsheet, you can get instant insights. A well-designed AI portfolio analyzer can:

- Highlight concentration risks automatically

- Evaluate sector diversification against benchmarks

- Identify which positions are driving performance

- Translate the numbers into plain-English insights

- Suggest specific improvements

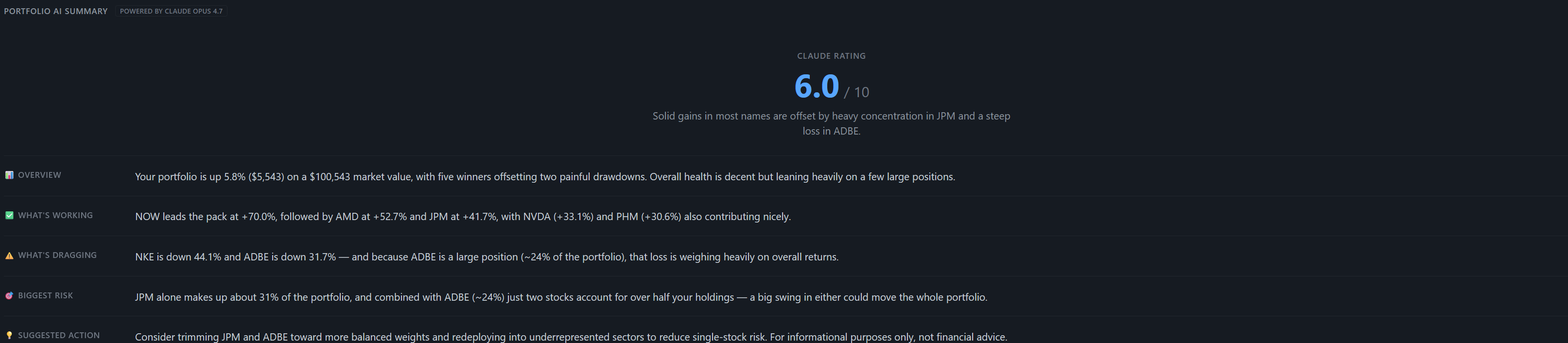

That's exactly what StockDashes does. You paste in your portfolio, and within seconds you get an AI-generated breakdown of what's working, what's risky, and what to consider changing, written like a friend explaining it to you, not a financial report.

Final Thoughts

A strong portfolio isn't just about returns. It's about balance, risk management, and smart allocation.

If you don't understand your portfolio, you're relying on luck. You might get away with it for years during a bull market. But eventually markets correct, and portfolios that were built on luck rather than strategy tend to fail at exactly the wrong time.

The investors who do well over decades aren't the ones picking the hottest stocks. They're the ones who understand what they own, know where their real risks are, and adjust calmly when conditions change.

FAQs

How often should I analyze my portfolio? A thorough analysis once a month is enough for most long-term investors. If you're more active, reviewing every two weeks keeps you aware of concentration drift. Always re-analyze after major events: earnings seasons, market corrections above 10%, or when you add a new position. Daily portfolio watching is usually counterproductive because it encourages emotional trading rather than strategic decisions.

What percentage of my portfolio should be in one stock? For most retail investors, no single stock should be more than 10-15% of the portfolio. The absolute ceiling should be 20-25%, and only for high-conviction positions you've deliberately sized up. If you inherited a concentrated position (employer stock, for example), consider reducing it gradually to avoid triggering large tax events.

What is a good diversification level? True diversification means no single stock dominates, no single sector is more than 40% of your portfolio, and your holdings don't all move in the same direction. A good benchmark is to compare your sector weightings to the S&P 500: tech 30%, healthcare 13%, financials 12%, and so on. Significant deviation from these weights represents a deliberate bet that you should be able to justify.

Can I analyze my portfolio without tools? Yes, but it's time-consuming. You'd need to calculate position weights, sector weightings, beta, correlations, and performance attribution in a spreadsheet. Most investors who try this give up after a few months. Tools that do this automatically aren't a luxury. They're the difference between actually analyzing your portfolio and pretending to.

Should I include my pension or retirement accounts in portfolio analysis? Yes, absolutely. Your pension and retirement savings are part of your total investment exposure, even if you can't actively trade them day-to-day. If your pension is heavily invested in a global equity fund and your brokerage account is also mostly stocks, you're much more concentrated in equities than you think. Analyze your total portfolio across all accounts to see the real picture.

How do I know if I'm taking too much risk? The honest test is whether you could tolerate a 30% drawdown without panic-selling. If your portfolio has dropped 10% and you're already losing sleep, you're taking more risk than you can handle emotionally. Emotional reactions during downturns are the single biggest destroyer of retail returns. Dial down risk until you can stay calm in a correction, not until markets are calm.

Try It Yourself

Skip the manual work. Get an instant AI breakdown of your portfolio at StockDashes.